Property Based Income for Retirees: Unlocking Real Estate Potential

Introduction:

Property based income for retirees can help retirement to be a time of financial freedom and peace of mind. But many retirees are looking for ways to top up their income. That’s where property based income strategies come in and can be a goldmine for those looking to secure their financial future in their golden years.

Whether you already own property or are thinking of investing, real estate can be an income generator. From traditional long term rentals to short term vacation homes and even creative options like renting out parking spaces the options are endless and fun.

But why should retirees consider property based income? Firstly it’s a way to diversify your retirement portfolio, a more stable tangible asset than some other investments. Real estate generally appreciates over time and can build long term wealth. And rental income can be a steady stream of cash flow on top of pensions or social security.

In this article we’ll look at property based income opportunities for retirees. We’ll cover different strategies, the benefits and the challenges you’ll face. By the end you’ll know how to use real estate to boost your retirement income.

So whether you’re a seasoned property owner or a newbie to real estate investing join us as we explore property based income in retirement. You never know you might just find a new way to financial freedom in your golden years.

Property Income for Retirees

Let’s face it retirement isn’t always the financial picnic we thought it would be. For many retirees, living on a fixed income means carefully managing expenses to avoid financial burdens. You’re staring at your bank account wondering how to stretch those dollars further. That’s where property based income comes in and boy can it be a game changer!

Why Real Estate for Retirees

I was talking to my neighbor Bob a few years ago and he was worried his retirement funds were disappearing faster than he thought. Fast forward to last week and there he was beaming from ear to ear telling me about the rental income from his duplex. It’s like he found a money tree in his backyard!

Now why is real estate income so attractive for retirees to us oldies? Well for starters it’s tangible. You can see it, touch it and even paint it if you feel like it. Unlike those mysterious stocks that go up and down faster than a yo-yo, property generally appreciates over time. And it can provide a steady stream of income more reliable than your grandkids promise to mow the lawn. Additionally, owning investment properties can diversify your income sources and offer tax benefits, making it a smart choice for retirees.

Passive Rental Income in Retirement

But here’s the kicker – passive income. Imagine sipping a piña colada on the beach while your property works for you. Sounds good right? That’s what real estate in retirement is like. It’s like having a part time job except you don’t have to wear pants or have a cranky boss.

Retirement rental income can be a significant financial asset, providing stability and potential tax benefits.

Of course it’s not all sunshine and rainbows. There are challenges too but we’ll get to those later. For now let’s focus on the good stuff. Property based income can be a buffer against inflation, unexpected expenses or just those impulse buys you can’t resist. (We’ve all been there, no judgment!)

So whether you want to supplement your pension, leave a legacy for your kids or just have some extra cash for that golf membership, property income might be your ticket to a more comfortable retirement. It’s like finding an extra gear in your financial engine – vrooom!

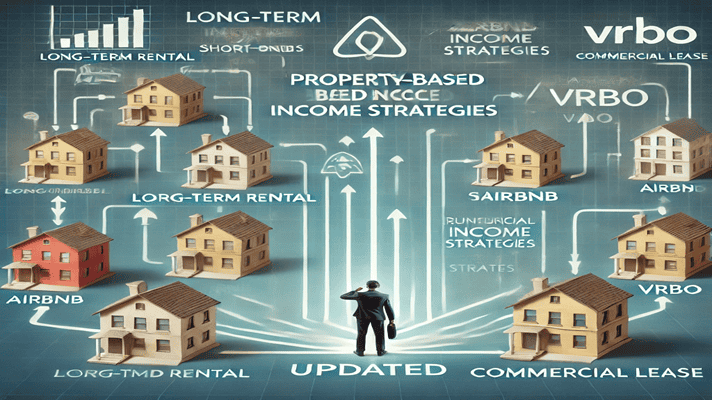

Property-Based Income Strategies

Okay folks let’s get into the good stuff – the different ways you can make your property work harder than a beaver building a dam. I mean there are more options than toppings at an ice cream parlor!

Long Term Rental Properties

First up we have long term rental properties. This is the classic “buy a house, rent it out” strategy. It’s like having tenants as your personal piggy bank, shaking out some coins every month. I knew a guy who started with one rental house and ended up with a mini-empire. He jokes that his tenants paid for his RV and his trip to Alaska! By acquiring a few rental properties, you can calculate the monthly cash flow needed to achieve financial stability and even plan for retirement.

Short Term Rentals and Vacation Homes

But maybe you’re thinking “I don’t want to deal with year long leases and tenant drama”. Well hold onto your dentures because short term rentals might be your thing. We’re talking Airbnb, VRBO, all that jazz. It’s like running a mini-hotel except you don’t have to wear one of those fancy uniforms.

Short-term rentals income can significantly contribute to a retirees monthly income, providing a steady stream of revenue from guests.

I gotta tell ya, my friend Sarah was hesitant at first. She had a spare room collecting dust like a library book that hadn’t been opened in years. But after listing it on Airbnb she’s now making enough to fund her pottery hobby and then some. She even enjoys being a tour guide for her guests!

Property Management Opportunities

Now if you’re more of a “behind the scenes” type, property management might be your thing. It’s perfect for those who love organizing things and bossing people around (in a nice way of course). You could manage other people’s properties and take a slice of the pie without owning the whole bakery.

Creative Property Income Ideas for Retirees

But wait there’s more! Ever thought of renting out your driveway for parking? Or your garage for storage? Heck I even heard of someone renting out their pool by the hour! The possibilities are endless, limited only by your imagination and local zoning laws (always check those, trust me).

The beauty of these strategies is you can mix and match. Maybe you have a long term rental property but rent out the garage separately. Or perhaps you do short term rentals during tourist season and switch to long term for the rest of the year. It’s like creating your own real estate cocktail – shaken, not stirred!

Remember the key is to find what works for you. Maybe you’re a people person who’d love interacting with Airbnb guests. Or perhaps you prefer the stability of long term rentals. There’s no one size fits all in this game. It’s all about finding your property groove!

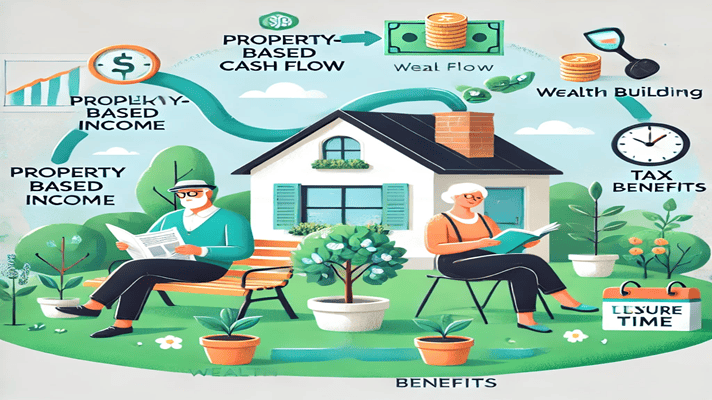

Property-Based Income in Retirement

Let’s get into the good stuff – the benefits of property-based income for retirees. Buckle up, we’re about to ride the benefits train! We’re not just talking about a little extra pocket money here – we’re talking about potentially changing your retirement lifestyle.

Maximizing income streams is crucial in retirement planning, as it can lead to reduced risks and enhanced financial security. Imagine having a steady stream of income that could fund those bucket list adventures or simply provide a cushion of financial security. It’s like finding a golden goose, except instead of eggs, it’s laying rent checks and property appreciation. So let’s get into the treasure trove of benefits that property based income can bring to your golden years!

Regular Cash Flow and Passive Income

First stop: Regular, passive income station. Imagine money rolling into your account every month as reliable as your old college roommate asking to borrow cash. That’s what rental income can be like. It’s like planting a money tree in your yard, except this one actually grows!

Understanding how much income is necessary to support different retirement lifestyles is crucial. This includes knowing the required income to maintain your desired lifestyle or to qualify for a mortgage.

I knew a retiree who used her rental income to fund a weekly poker night. She says she’s not gambling – she’s “reinvesting her property profits.”

Property Appreciation and Wealth Building

Next up we’ve got the asset appreciation express. Over time properties tend to increase in value. It’s like your house is at the gym, pumping iron and getting more valuable while you kick back and relax. My buddy Tom bought a fixer upper ten years ago. Today it’s worth more than his original retirement savings! Talk about a home run.

Tax Benefits for Property Owners

Now let’s not forget the tax advantages tunnel. Uncle Sam actually gives you some breaks for being a property owner. You can deduct things like mortgage interest, property taxes and maintenance expenses. It’s like the government is chipping in for your property upkeep. Who knew taxes could be exciting?

Flexibility and Portfolio Diversification

Last but not least we’ve got flexibility junction. With property investments you can be as involved or hands off as you want. Feel like being a landlord? Go for it! Rather hire a property manager and sip margaritas? That works too! It’s like choosing your own adventure, retirement edition.

But here’s the real kicker – diversification. When retirees add property income to their retirement portfolio they’re not putting all their eggs in one basket. It’s like having a financial safety net, just in case the stock market decides to do the cha-cha.

Of course it’s not all rainbows and unicorns. There are challenges too, which we’ll get into later. But for now let’s bask in the glow of these benefits. It’s like finding out chocolate is a health food – too good to be true, but it actually kind of is!

Remember though, everyone’s situation is different. What works for your golf buddy might not work for you. It’s all about finding the right fit for your retirement puzzle. But with these benefits, property based income might just be the piece you’ve been looking for!

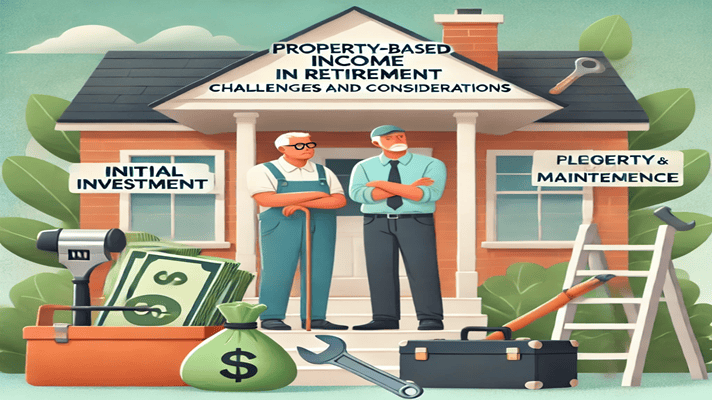

Challenges and Considerations

Okay folks, it’s time to take off those rose colored glasses and look at the potential pitfalls in our property income plans for retirees. Don’t worry, I’m not here to rain on your parade, just to make sure you bring an umbrella! After all being prepared is half the battle when it comes to real estate investing.

Think of these challenges as the pop quiz before the big exam – they might seem daunting at first but tackling them head on will make you a savvier investor in the long run. So let’s roll up our sleeves and get into the nitty gritty of what you might face on your property income journey.

Initial Investment and Ongoing Costs

First up let’s talk about the elephant in the room – money. Getting started with senior property investments can cost more than your grandkid’s college tuition. You’ve got the down payment, closing costs and maybe some renovations to boot. It’s like trying to fill a swimming pool with a garden hose – it takes time and a lot of water!

When qualifying for loans, lenders typically require a low debt-to-income ratio to secure favorable terms. This ratio is crucial as it reflects your overall financial health and borrowing capacity.

Then there’s the ongoing costs. Property taxes, insurance, maintenance – it’s like your property has a never ending shopping list. I remember when my buddy Joe got his first rental property. He was so excited until the water heater broke, the roof started leaking and the tenant’s dog ate the carpet – all in the first month! Poor Joe looked like he’d aged ten years in four weeks.

Property Maintenance and Management

And speaking of maintenance, that’s a whole can of worms right there. If you’re handy with a toolbox, great! If not, get ready to have your plumber and electrician on speed dial. It’s like playing whack-a-mole with house problems sometimes.

Market Fluctuations and Economic Factors

And let’s not forget about those pesky market fluctuations. The real estate market can be as unpredictable as a cat on catnip. One minute you’re riding high on appreciating values, the next you’re wondering if you should’ve invested in a giant jar of pennies instead.

Legal and Regulatory Considerations

And then there’s the legal stuff. Oof, don’t get me started on the legal stuff. Tenant laws, zoning regulations, tax codes – it’s enough to make your head spin faster than a ceiling fan. You might need to get cozy with a lawyer and an accountant, which isn’t exactly most people’s idea of a fun Friday night.

There are various mortgage loan options available to retirees, including government programs and specific lending criteria that consider income sources like Social Security.

But here’s the thing – these challenges aren’t deal breakers. They’re more like speed bumps on the road to property income success. With some planning, patience and maybe a little luck you can navigate these hurdles.

Every investment has risks. The key is to go in with your eyes wide open. Do your homework, crunch the numbers and maybe start small. Rome wasn’t built in a day and your real estate empire doesn’t have to be either.

In the end it’s all about balancing the potential rewards with the risks and responsibilities. It’s like deciding whether to eat that extra slice of pie – sure there might be consequences but boy can it be worth it!

Getting Started with Property-Based Income

Okay future real estate moguls, let’s get started with dipping your toes into the property income pool. Don’t worry, I promise the water’s fine… most of the time!

Assessing Your Financial Situation

First things first you gotta take a good hard look at your financial situation. It’s like checking yourself out in the mirror before a big date – you wanna know what you’re working with! How much can you invest? What’s your risk tolerance? Are you looking for long term growth or immediate income? These are the questions you need to answer before you start browsing those real estate listings.

Researching Local Real Estate Markets

Now it’s time to channel your inner Sherlock Holmes and do some detective work in your local real estate market. What areas are up-and-coming? Where are the good schools? (Trust me, parents will pay top dollar to be in a good school district!) What’s the job market like? You’re basically trying to predict the future which is about as easy as nailing jelly to a wall. But hey, that’s part of the fun!

Exploring Property Investment Options for Retirees

Now let’s talk about your options. There’s more ways to invest in property than there are flavors at a fancy ice cream shop. You’ve got your traditional buy-and-rent properties, fix-and-flip opportunities, real estate investment trusts (REITs) and even crowdfunding platforms. Rental real estate is a particularly attractive option, offering passive income and financial stability for retirement as tenants cover expenses. It’s like a buffet of real estate options – try a little of everything and see what suits your taste!

Leveraging Resources and Professional Help

But here’s the kicker – you don’t have to go it alone. There’s a whole world of resources out there to help you learn the ropes. Books, podcasts, online courses – heck I even knew a guy who learned everything he knows about property management from YouTube videos! (Okay maybe don’t rely entirely on YouTube but you get the idea.)

Local real estate investor groups are a goldmine of information and networking opportunities. It’s like joining a book club, except instead of discussing the latest bestseller you’re swapping tips on how to deal with nightmare tenants.

And don’t be afraid to reach out to professionals. A good real estate agent, property manager or financial advisor can be worth their weight in gold. Sure they might cost a pretty penny but so do rookie mistakes in the real estate game.

Start Out Small

Understanding other retirement income is crucial for financial planning and securing loans. Seeking professional advice can help you navigate the complexities of various income streams and their tax implications.

Remember, starting small is okay. You don’t need to buy a whole apartment complex right off the bat. Maybe you start by renting out a room in your house or partnering with a friend on a small property. It’s like learning to swim – you start in the shallow end before diving into the deep stuff.

The most important thing is to just start. Take that first step, make that first investment, sign that first lease. Will you make mistakes? Probably. Will you learn from them? Absolutely. And before you know it you’ll be sharing your own property income war stories with the grandkids.

So there you have it, folks. Your roadmap to getting started with property-based income. It might seem overwhelming now but remember – every real estate tycoon started somewhere. Who knows? This time next year you could be sipping cocktails on the beach all thanks to your property investments. Now wouldn’t that be something?

Conclusion:

As we finish up our property-based income strategies for retirees it’s clear that real estate can be a valuable way to supplement retirement income and build long term wealth. Whether through traditional rentals, short term hosting or property management these strategies can provide a steady income stream and asset appreciation.

But remember property investment isn’t a one size fits all solution. Every retiree is unique and what works for one won’t work for another. You need to carefully consider your options, understand the responsibilities involved and seek professional advice when needed.

The benefits of property-based income in retirement are many. From regular cash flow to tax advantages, from asset appreciation to portfolio diversification real estate can add a whole new dimension to your retirement plan. But equally you need to be aware of the challenges – initial investment, ongoing costs and market fluctuations.

As you weigh your options remember it’s never too late to start. Whether you’re just starting your retirement journey or you’ve been enjoying your golden years for a while there’s always room for new opportunities and adventures in real estate.

Consider starting small, maybe by renting out a spare room or partnering with a friend on a small property. Leverage your existing resources and don’t be afraid to seek professional advice. With planning and research property-based income strategies could be the key to a more financially secure and enjoyable retirement.

Your property-powered retirement awaits. Are you ready to turn that key?

Disclosure: Some of the links in this article may be affiliate links, which can provide compensation to us at no cost to you if you decide to purchase. This site is not intended to provide financial advice. You can read our affiliate disclosure in our privacy policy.